Breville Group (ASX:BRG): Forecast & Valuation

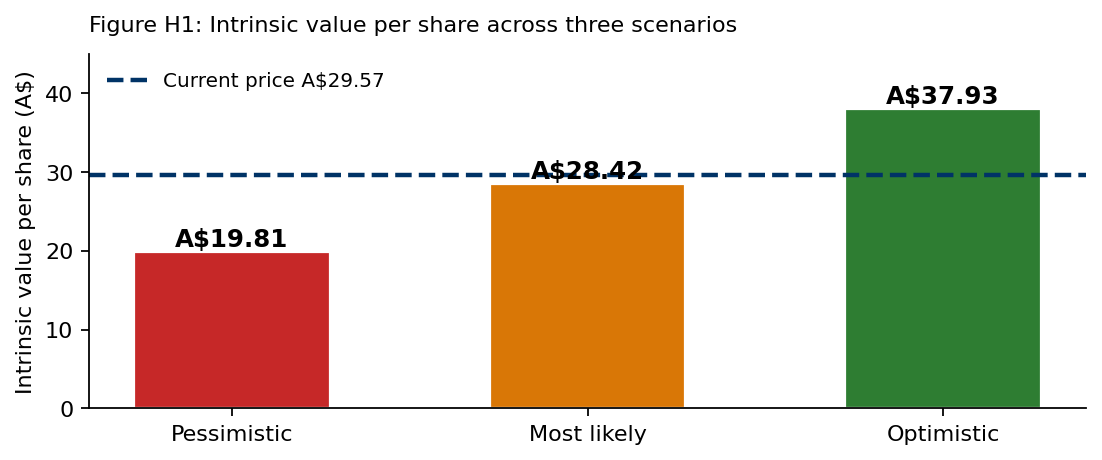

Built a full forecast and discounted-cash-flow valuation of Breville Group (ASX:BRG) for a Monash valuation subject: a 12-year FCFE model across three scenarios, landing on a HOLD with an intrinsic value of A$28.42 against a A$29.57 market price.

- Role

- Equity Valuation, Monash ACX3150

- Organisation

- Monash University

- Location

- Melbourne, Australia

Includes the full report (Word) and the valuation model (Excel).

Valuation scenarios

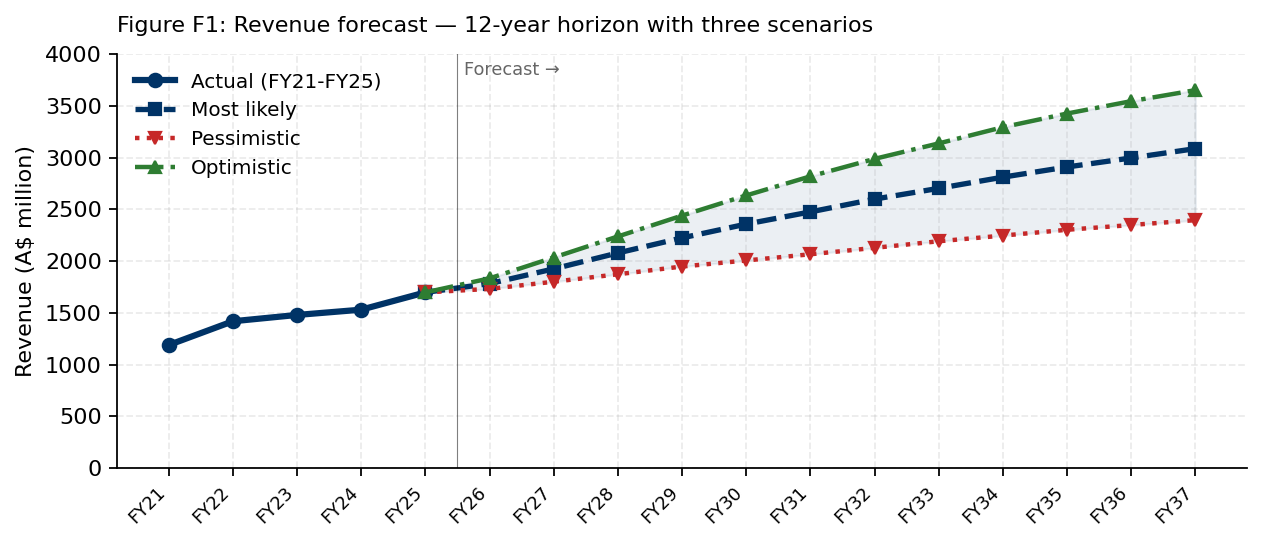

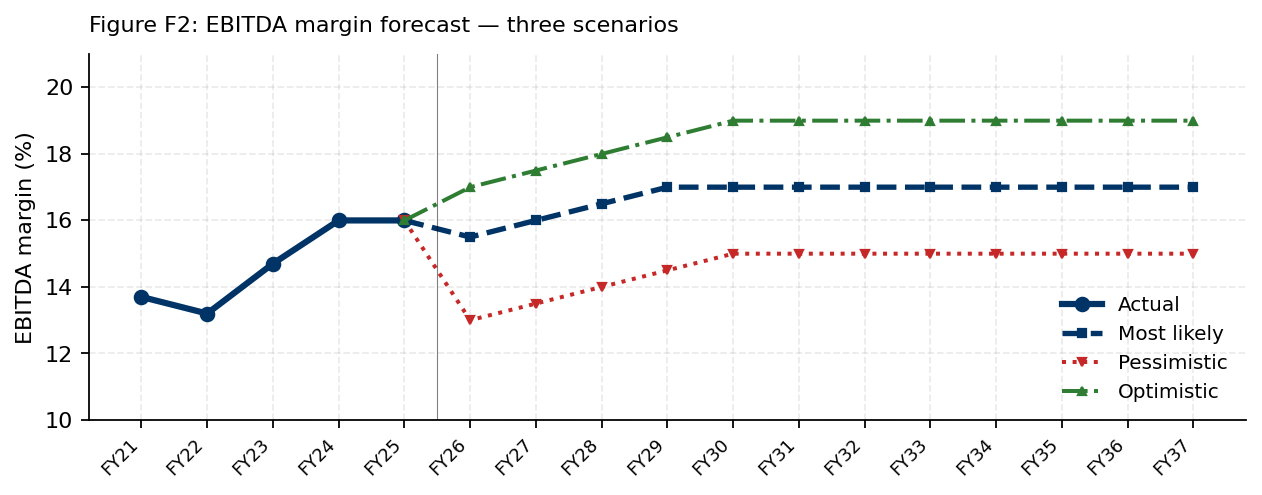

Tariffs persist and demand softens; steady-state EBITDA margin holds at 15%.

Manufacturing shifts out of China on plan; margin recovers to 17%.

Diversification is accretive and Coffee keeps growing; margin reaches 19%.

For a Monash valuation subject (ACX3150) I built a full forecast and discounted-cash-flow valuation of Breville Group, the ASX-listed premium appliance maker. The model lands on a HOLD: an intrinsic value of A$28.42 per share against a A$29.57 market price. You can download the full report and model below.

Context

Breville designs and markets premium kitchen appliances and outsources the manufacturing, so it runs an asset-light model. Two things made it interesting to value in 2026: US tariffs were pushing up landed costs on China-made product, and the company was part-way through moving its US sourcing out of China. Both feed straight into margins and the forecast.

Accounting analysis

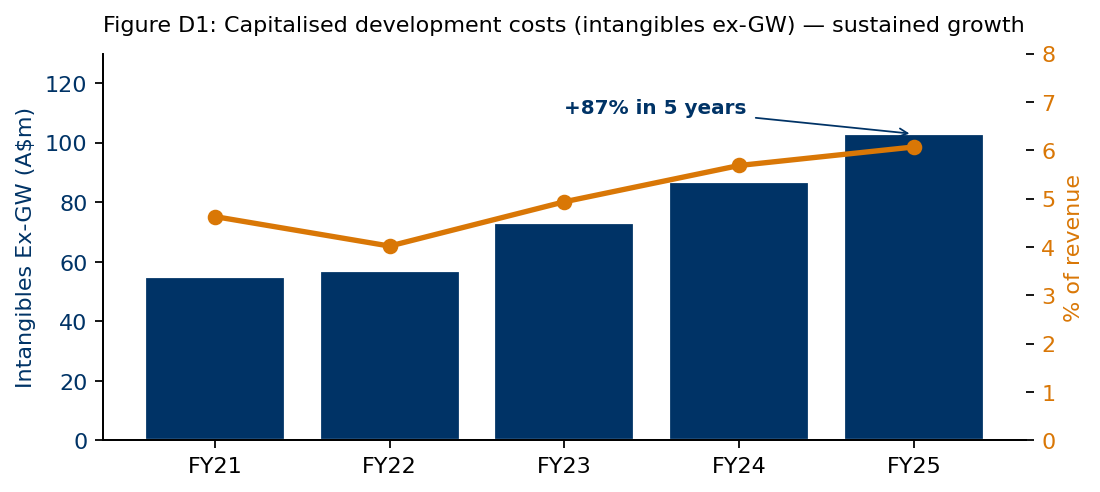

I started by checking the accounting quality, since that is where reported profit can be flattered. Three policies do most of the work: capitalised development costs, inventory, and goodwill.

The clearest flag is capitalised development costs. Intangibles (excluding goodwill) grew 87% over five years, faster than revenue. That is defensible given the company's product-led strategy, but capitalising rather than expensing flatters current profit, and the rising amortisation will slow future earnings.

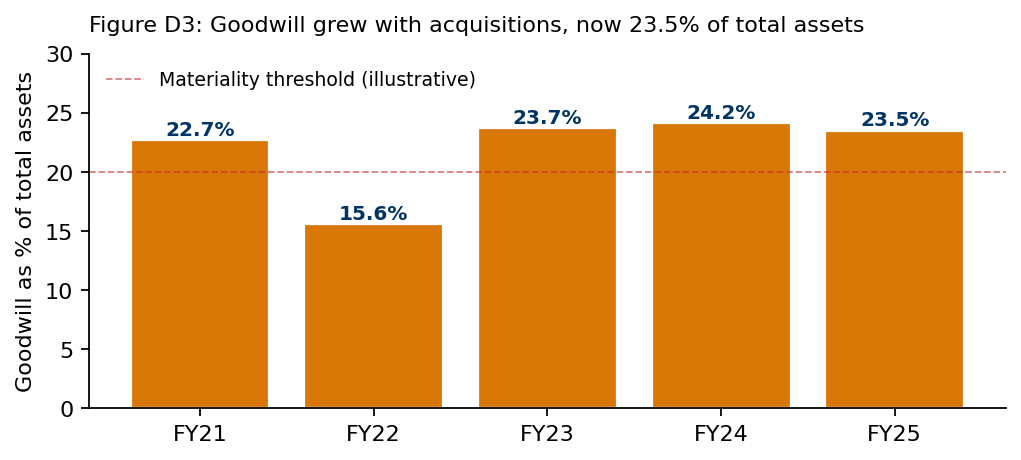

Goodwill from recent acquisitions now sits at 23.5% of total assets. It is not amortised, only tested for impairment, and that test leans on management's growth assumptions. With the US business under tariff pressure, this is the most likely place a future write-down would show up.

Financial analysis

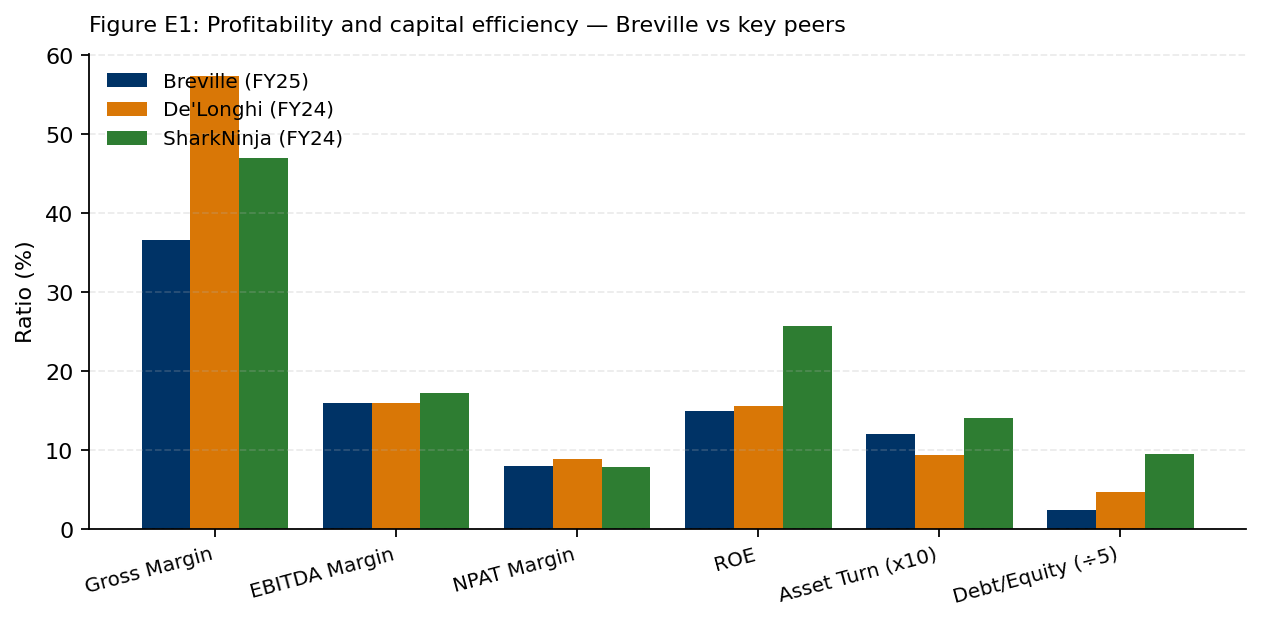

I benchmarked Breville against two listed peers, De'Longhi and SharkNinja. Breville sits between them on most operating measures and is the cleanest of the three on the balance sheet, with debt-to-equity of just 12%. Its lower return on equity is a leverage choice, not weaker operations: return on assets is mid-pack.

Forecast

I forecast a 12-year explicit horizon (FY26 to FY37) plus a terminal year, using an eight-driver model (sales growth, EBITDA margin, working capital, capex, debt, and so on) and discounting free cash flow to equity. Revenue grows from about A$1.7bn to A$3.1bn in the most-likely case, fading toward the industry growth rate.

The margin assumption does most of the work. I have EBITDA margin dipping in FY26 as residual tariff cost lands, then recovering to a 17% steady state as sourcing moves to lower-cost countries and scale builds.

I built three scenarios rather than one. The downside takes 300bps off the steady-state margin while the upside adds 200bps, because the recent tariff and demand shocks point to more risk on the way down than the way up.

Cost of capital

I discounted at a cost of equity of 8.98%, using CAPM with a 0.78 beta, a 4.3% risk-free rate, and a 6% equity risk premium. The beta below 1 fits an established brand with a conservative balance sheet, and the same rate applies across all three scenarios since the underlying business risk does not change.

Valuation and recommendation

The most-likely case values Breville at A$28.42 per share, about 4% below the A$29.57 market price, which puts it in HOLD territory. The scenario range above shows how much rides on the margin and growth assumptions. The main catalysts that would move it to a buy are the manufacturing shift staying on track and the Coffee category continuing to grow; a re-escalation of tariffs or inventory write-downs would push it toward a sell.

What I took from it

A valuation is only as good as the assumptions you can defend. The input that mattered most here was the steady-state EBITDA margin: a 100bps change moves the value by about A$2.50 a share, so most of the work went into justifying that one number rather than polishing the model.